Railroad Retirement Board Benefits and Medicare

Before the Social Security Administration (SSA) was formed, the Railroad Retirement Board (RRB) developed retirement, disability, and unemployment benefits for railroad workers who were hit hard by the Great Depression. Today, the RRB offers railroad workers a similar safety net.

RRB beneficiaries can tap into Medicare benefits, much like Social Security beneficiaries, with a few differences. If you are a railroad worker, learn what you can expect from Medicare in terms of eligibility, enrollment, costs, and health benefits—and how your RRB benefits differ from Social Security benefits.

Eligibility and enrollment

When you become eligible for Medicare benefits is similar for both RRB and SSA. Typically, you’ll become eligible when you turn 65 or reach your 25th month of receiving disability benefits. The main difference is that the RRB classifies disability differently than the SSA does, so check with a representative at your nearest RRB field office to ensure you qualify.

Due to COVID-19, the Railroad Retirement Board closed offices as of March 16, 2020. We’ll keep you updated on when offices reopen. In the meantime, visit RRB.gov to learn about your online self-serve options.

How do I enroll?

Most railroad workers enroll in Medicare by contacting their local Railroad Retirement Board office. You can find the nearest office using the field office link above. But if you have end-stage renal disease, you must enroll through the Social Security Administration.

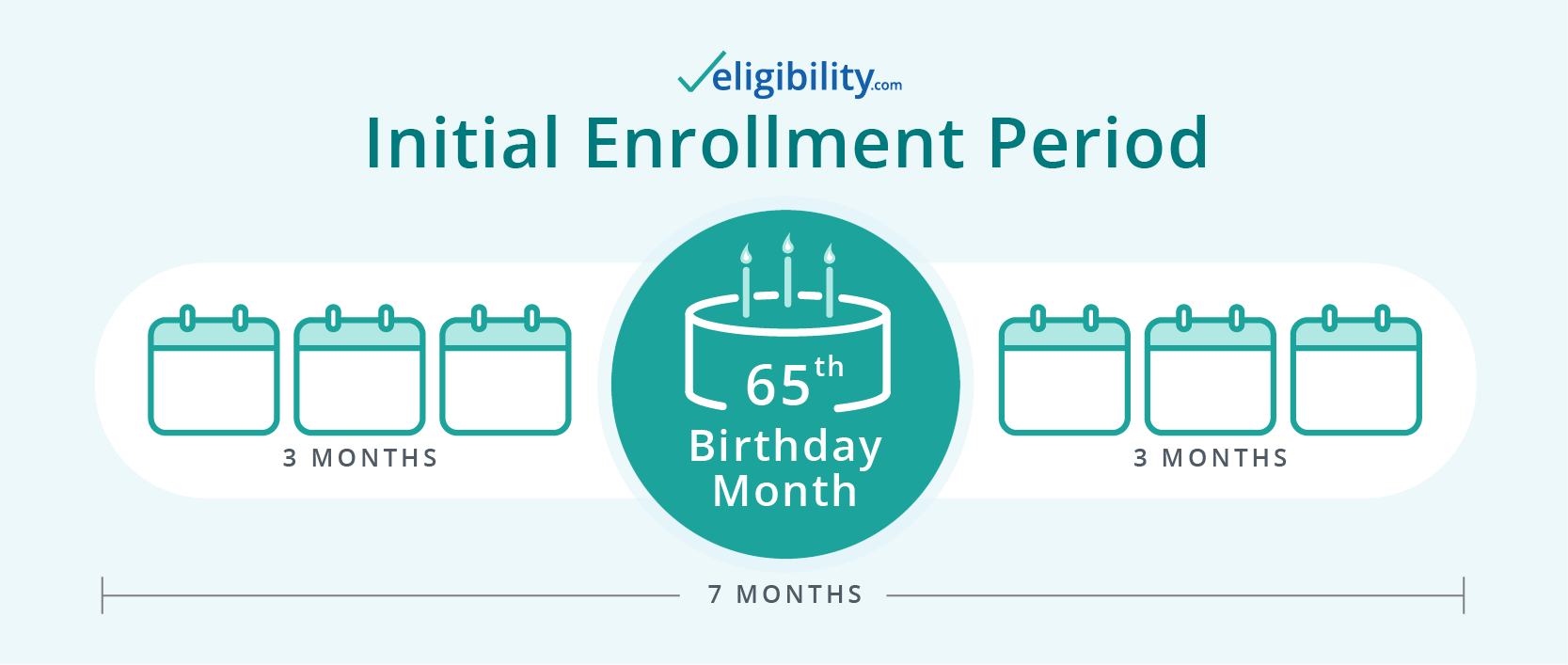

Whether you become eligible for Medicare via age or disability, you’ll have seven months, called your Initial Enrollment Period (IEP), in which to enroll. This period begins three months before and ends three months after you become eligible for benefits. (Remember, that’s when you turn 65 or during your 25th month receiving RRB disability income.)

If you’re approaching eligibility, get started as soon as possible. If you miss your enrollment period, you could rack up late-enrollment penalties—and have to wait until the beginning of the following year to enroll.

What if I receive a surprise Medicare card in the mail?

People who qualify for Medicare due to disability and those who begin receiving retirement benefits before turning 65 may be automatically enrolled in Medicare.

If that’s you, congratulations! Your enrollment is complete, and now you can decide whether you want to add additional coverage, such as Part D prescription drug coverage or Medigap. Or you can choose a Medicare Advantage plan, which could add benefits such as dental, vision, and prescription coverage.

If you receive a surprise Medicare card in the mail and don’t want the coverage, you may be able to cancel Part B. Be aware, however, that disenrolling now could mean incurring late-enrollment penalties in the future. You can also cancel Part A, but most people who receive premium-free Part A keep this coverage because it doesn’t cost them anything.

Learn how to disenroll from Medicare Part B.

Costs

Generally, your Medicare costs through the RRB will be the same as those paid by people who qualify for Medicare via Social Security. Just like workers outside the railroad industry, you’ll see Medicare deductions from your paycheck during your working years. These are the same for all workers: 1.45% of your income in 2020.1

These payments go toward earning premium-free Part A, which you’ll qualify for after working and paying Medicare taxes for a total of 10 or more years (40 quarters). If you don’t work that long, you may have to pay for Part A—up to $458 in 2020.2

For Part B, you’ll pay the same premium as other Medicare recipients. The standard Part B premium is $198 in 2020, but if your individual annual income is $85,000 or higher, you could pay more.3 This monthly premium will come straight out of your RRB income check if you’re receiving those benefits.

If you add Medicare Part D, Medigap, or Medicare Advantage, you’ll pay additional premiums for these as well, but not through your RRB income checks. You’ll pay for each of these coverages separately, directly to the insurance company that provides each plan.

Benefits

Generally, Medicare benefits are the same whether you qualify via Social Security or the Railroad Retirement Board. But there are a few differences.

Family coverage

With railroad Medicare, more of your family members could qualify for coverage based on your working record. All Medicare beneficiaries’ spouses, divorced spouses, and surviving spouses may be eligible for Part A benefits. But railroad workers can add dependent parents to that list too.

Billing

Doctors will bill you differently for Part B covered expenses. The Railroad Retirement Board uses its own billing contractor, and your doctor can’t bill Medicare directly. Ensure your doctors know you have RRB Medicare benefits. While your Medicare card will say so, it never hurts to double-check to avoid payment delays.

Benefits in Canada

Generally, Medicare doesn’t cover health care costs in foreign countries, but RRB beneficiaries can use Medicare Part A for covered hospital expenses incurred in Canada. However, you may not receive coverage for Part B medical expenses, such as doctor visits, lab work, and preventative care.

Make the most of your railroad Medicare benefits

Railroad Retirement Board benefits are a lot like Social Security benefits. Your Medicare benefits are generally the same as well, except for a few perks. For example, you may be able to obtain coverage under Part A in Canada, and you may be able to cover dependent parents based on your work record instead of theirs.

Another thing that doesn’t change for RRB beneficiaries? How we can help. No matter how you earn your Medicare benefits, we can help you understand those benefits and help you get the best coverage for your situation. So, give us a call.

Sources:

1. Internal Revenue Service, “Topic No. 751 Social Security and Medicare Withholding Rates”

2. Medicare, “Medicare Costs at a Glance”

3. Medicare, “Medicare Costs at a Glance”

Content on this site has not been reviewed or endorsed by the Centers for Medicare & Medicaid Services, the United States Government, any state Medicare agency, or any private insurance agency (collectively "Medicare System Providers"). Eligibility.com is a DBA of Clear Link Technologies, LLC and is not affiliated with any Medicare System Providers.